India Milkshake Market Size, Share, Trends and Forecast by Flavor, Packaging, Distribution Channel, and Region, 2026-2034

India Milkshake Market Size, Share, Trends & Forecast (2026-2034)

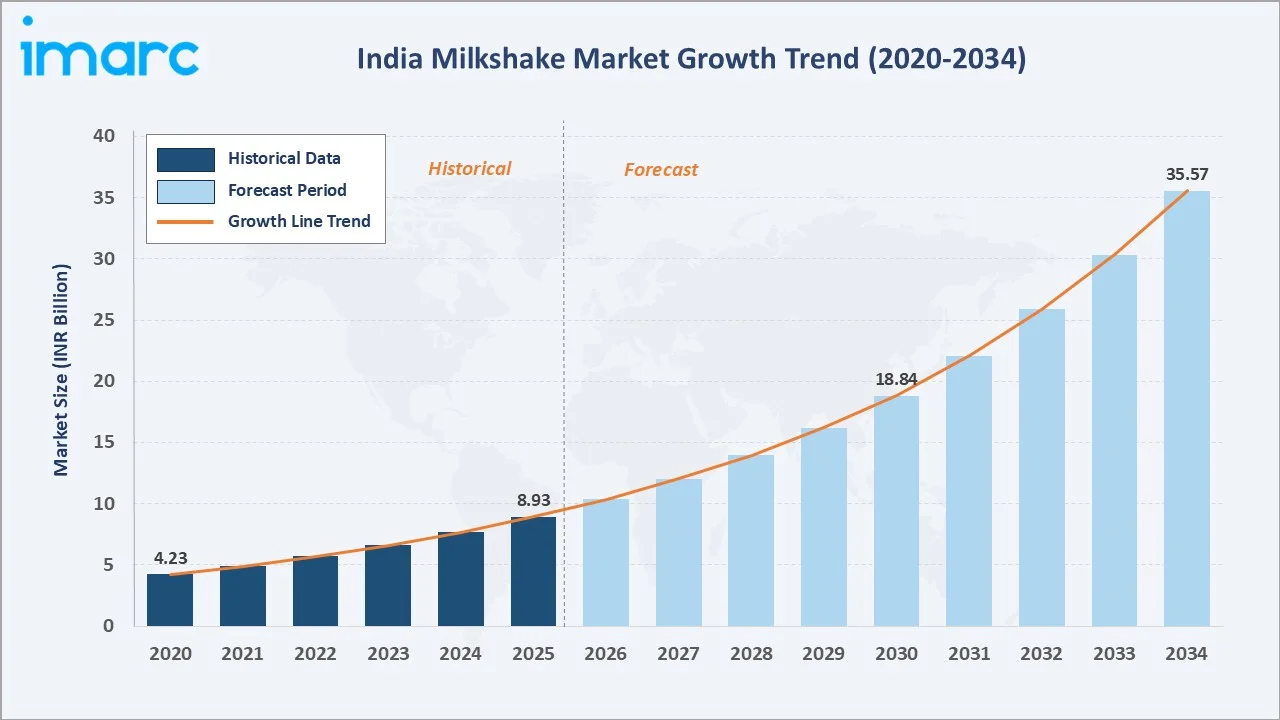

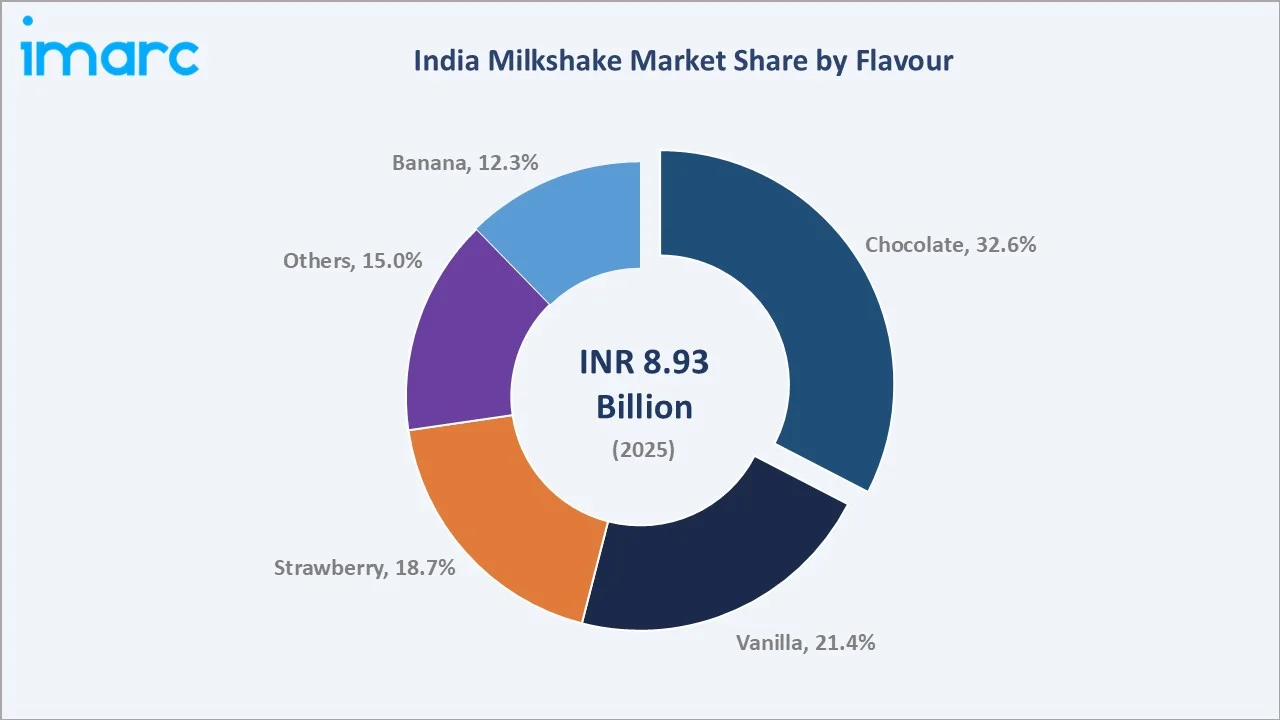

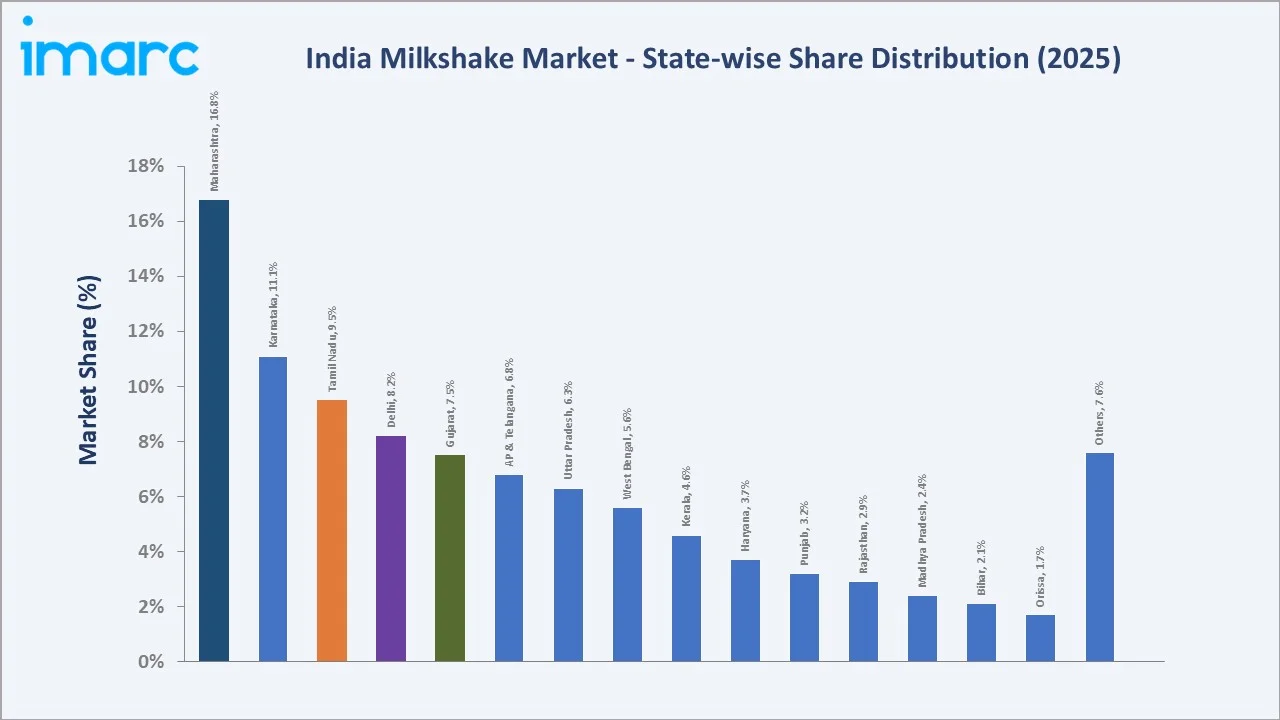

The India milkshake market size was valued at INR 8.93 Billion in 2025 and is projected to reach INR 35.57 Billion by 2034, exhibiting a CAGR of 16.10% during the forecast period 2026-2034. Rising urban youth consumption, expanding quick-commerce and online retail penetration, premium flavour innovation, and rising disposable in𒅌come are driving the India milkshake market growth. Chocolate leads the flavour segment at 32.6% in 2025, while Online Stores dominate the distribution channel at 28.4%. Maharashtra accounts for 16.8% of national revenue in 2025, the largest state-level market in India for milkshakes.

Market Snapshot

|

Metric |

Value |

| Market Size (2025) | INR 8.93 Billion |

| Forecast Market Size (2034) | INR 35.57 Billion |

| CAGR (2026-2034) | 16.10% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Largest State | Maharashtra (16.8% share, 2025) |

| Fastest Growing State | Maharashtra, supported by urban consumption |

| Leading Flavour | Chocolate (32.6%, 2025) |

| Leading Distribution Channel | Online Stores (28.4%, 2025) |

To get more information on this market, Request Sample

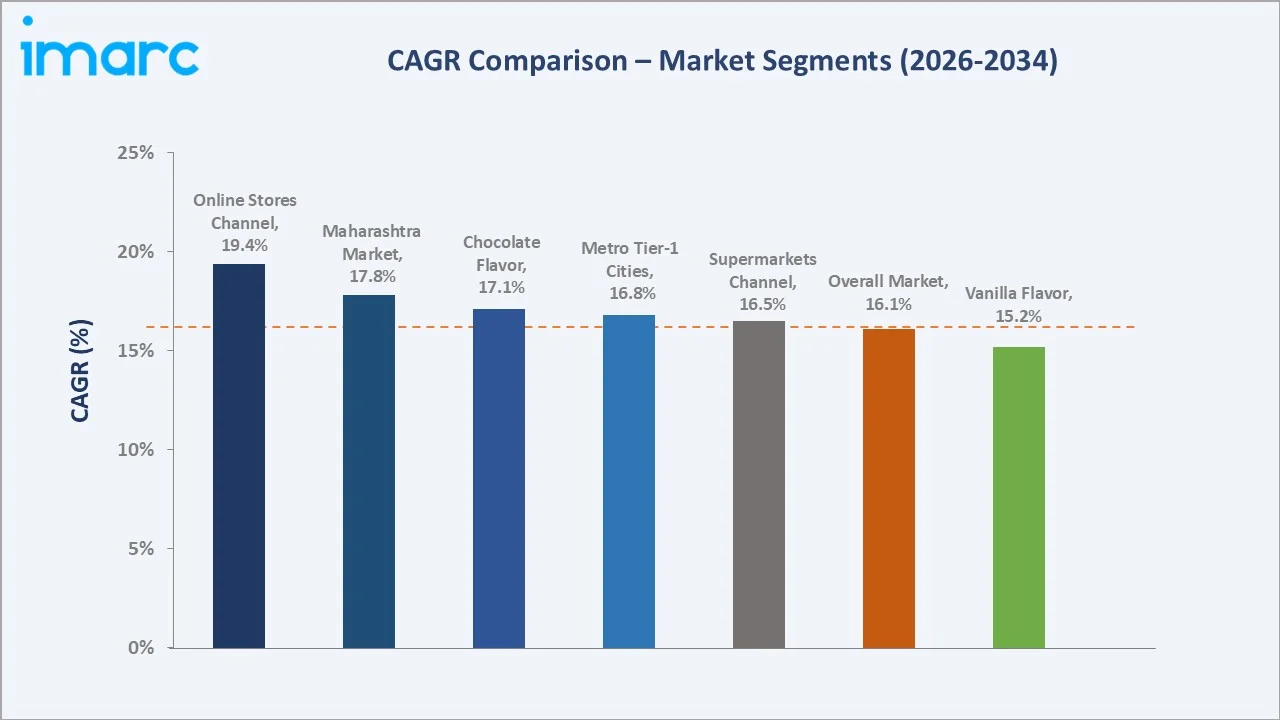

Segment-level CAGR comparison highlights online stores and Maharashtra as the two fastest-growing sub-segments within the India milkshake industry analysis through 2034, supported by quick-commerce expansion and premium urban consumption.

Executive Summary

Key Market Insights

|

Insight |

Data |

| Largest Flavour | Chocolate - 32.6% share (2025) |

| Largest Distribution Channel | Online Stores - 28.4% share (2025) |

| Leading State | Maharashtra - 16.8% revenue share (2025) |

| Second State | Karnataka - 11.1% revenue share (2025) |

| Top Companies | Amul (GCMMF), Mother Dairy Fruit & Vegetable Pvt. Ltd., Parle Agro, Britannia Industries, HAP (Hatsun Agro Product Limited), Heritage Foods Limited, Keventers, Cream Bell (Devyani Food Industries Ltd.) |

Key analytical observations supporting the above data:

- Chocolate's 32.6% dominance in 2025 reflects strong cultural appeal among Indian youth, broad retail availability across all channels, and consistent demand across urban metros, tier-2 cities, and aspirational tier-3 markets.

- Online Stores share at 28.4% in 2025 reflects the rapid growth of quick-commerce platforms, including Zepto, Blinkit, and Swiggy Instamart, which deliver chilled milkshakes within minutes, reshaping category consumption patterns.

- Maharashtra's 16.8% state share in 2025 reflects its leading urban population across Mumbai and Pune, mature organised retail ecosystem, strong dairy brand presence, and highest quick-commerce infrastructure density in India.

India Milkshake Market Overview

Market Dynamics

To evaluate market opportunities, 高清体育直播:Request Sample

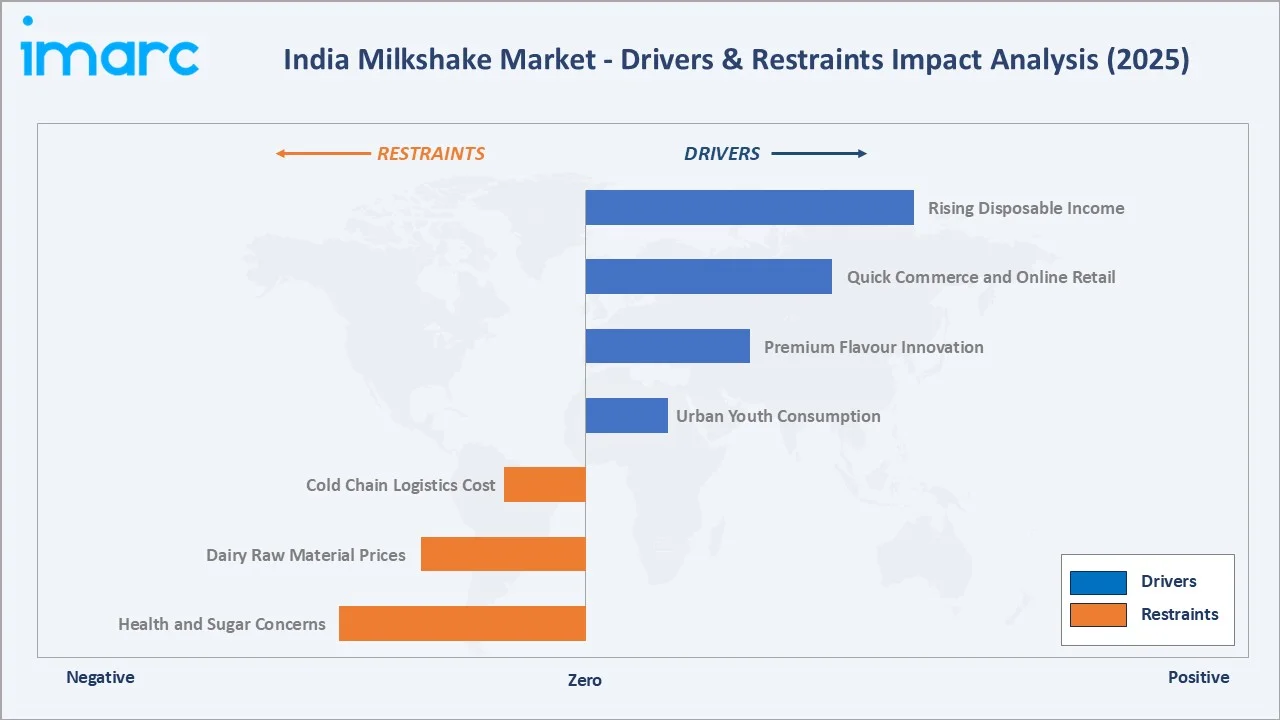

Market Drivers

- Urban Youth Consumption: India's urban population under age 35 represents a large, brand-conscious consumer base with a strong affinity for flavoured dairy beverages, driving sustained milkshake category growth across metros and tier-2 cities.

- Quick Commerce and Online Retail: Rapid expansion of quick delivery platforms, including Zepto, Blinkit, and Swiggy Instamart, has unlocked impulse chilled-beverage consumption at scale, significantly boosting milkshake discoverability and volume. India's quick commerce sector reached a gross order value of approximately ₹64,000 crore in 2025, driven by evolving consumer preferences, which is directly accelerating milkshake demand among urban consumers.

- Premium Flavour Innovation: Brands are launching indulgent and regional flavour variants (kesar-pista, cold coffee, kulfi-inspired) to capture premium spending, supporting average selling price growth and category differentiation. In June 2024, Ball Corporation partnered with CavinKare to introduce retort aluminium cans for its milkshake flavours, including Badam, Gulkhand, Rajbog, and Rabri, enhancing shelf life and sustainability for the premium RTD segment.

- Rising Disposable Income: Sustained growth in per-capita disposable income across urban and semi-urban India is enabling regular discretionary spending on branded beverages, supporting both volume expansion and premiumisation.

Market Restraints

- Cold Chain Logistics Cost: Chilled distribution infrastructure is expensive and uneven across India, particularly in tier-3 cities and rural markets, creating supply constraints and limiting category penetration beyond metropolitan hubs.

- Dairy Raw Material Prices: Volatility in milk procurement prices, sugar costs, and flavour ingredients exposes manufacturer margins to commodity cycles, with frequent need for selective price hikes that can dampen price-sensitive demand.

- Health and Sugar Concerns: Rising consumer awareness of added sugar, artificial flavours, and high-calorie content is creating headwinds for traditional sweet variants, pushing manufacturers to reformulate toward low-sugar and fortified alternatives.

Market Opportunities

- Plant-Based and Lactose-Free Milkshakes: Oat, almond, soy, and lactose-free dairy-based milkshakes are gaining traction among urban health-conscious consumers, opening a premium sub-segment with strong margin and brand-positioning potential. In June 2025, fitness brand HRX launched plant-based oat milk protein shakes in India, 100% dairy-free and lactose-free, available nationwide via Swiggy Instamart, Amazon, and Zomato.

- Functional and High-Protein Variants: Protein-enriched, vitamin-fortified, and performance-positioned milkshakes targeting students, office-goers, and fitness consumers represent a fast-growing segment supported by rising health and wellness spending.

- Regional and Artisanal Flavour Expansion: India-specific flavours such as kesar-pista, rose, mango, and jaggery-based shakes allow brands to connect with local palates and differentiate against global flavour profiles in competitive urban markets.

Market Challenges

- Intense Price Competition: Entry of regional dairy brands, private-label supermarket SKUs, and local parlour brands is intensifying pricing pressure, particularly at the INR 20-40 price point critical to impulse purchases.

- Short Shelf Life and Spoilage Risk: Chilled milkshake SKUs typically carry a short shelf life, requiring tight supply chain discipline and creating risk of stock loss across retail shelves, especially in smaller format stores.

Emerging Market Trends

1. Plant-Based and Lactose-Free Alternatives

Oat, almond, and soy-based milkshake variants are entering mainstream urban retail, targeting lactose-intolerant and health-conscious consumers. Brands are positioning plant-based options as premium offerings with clean-label credentials and sustainability messaging.2. Quick Commerce Channel Expansion

Ten-minute delivery platforms have fundamentally reshaped chilled beverage discovery in metros, with Zepto, Blinkit, and Swiggy Instamart driving significant milkshake category growth. This channel is becoming primary for impulse purchases among young urban consumers.3. Premium and Artisanal Brand Growth

Premium artisanal milkshake brands and thick-shake quick-service chains such as Keventers, Frugurpop, and Haagen-Dazs counters are expanding aggressively in metros, elevating category perceptions and driving trade-up behaviour. In March 2026, Keventers appointed a new CEO and announced plans to launch 70 new outlets within the year, targeting a tripling of its business over three years, actively diversifying into FMCG, quick commerce, and institutional sales as part of a broader ambition targeting younger Indian consumers.4. Low-Sugar and Functional Shakes

Reformulated low-sugar, zero-added-sugar, and protein-fortified milkshakes are gaining visibility in response to rising diabetes awareness and fitness culture. These variants command price premiums of 15-25% over standard SKUs.5. Regional Flavour Innovation

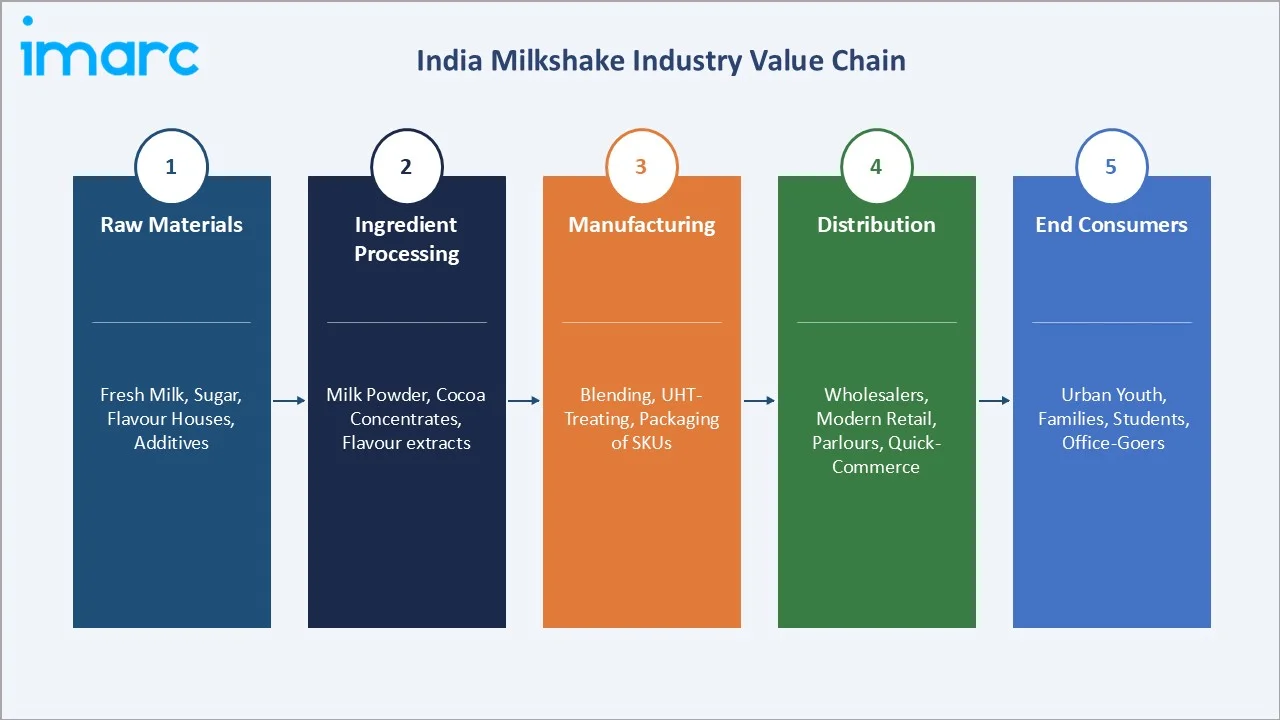

Indian heritage flavours, including kesar-pista, rose, kulfi, thandai, and jaggery, are being reimagined as packaged milkshake variants, enabling national brands to capture regional preferences while differentiating against global flavour profiles.Industry Value Chain Analysis

|

Stage |

Key Players / Examples |

| Raw Materials | Dairy cooperatives supply fresh milk, while sugar refiners, flavour houses, and additive makers provide sweeteners, stabilisers, and emulsifiers. |

| Ingredient Processing | Raw inputs are converted into beverage-grade milk powder, cocoa concentrates, and flavour extracts ready for consistent large-scale formulation. |

| Manufacturing | Branded producers blend, pasteurise or UHT-treat, homogenise, and package finished milkshake SKUs across chilled and ambient beverage formats. |

| Distribution | Finished products move from factory warehouses through wholesalers, organised retail chains, convenience outlets, milk parlours, and quick-commerce delivery platforms. |

| End Consumers | Urban youth, family households, and office and student segments across metros and tier-2 cities drive milkshake consumption demand. |

Technology Landscape in the India Milkshake Industry

Dairy Processing and Formulation

Indian manufacturers are adopting advanced UHT and aseptic processing technologies that extend shelf life, support ambient distribution, and enable wider geographic reach. Spray-dried dairy powders and stabilised emulsions support flavour consistency across long supply chains.Flavour and Ingredient Innovation

Natural flavour extracts, low-glycaemic sweeteners (stevia, monk fruit), and functional additives (plant protein, vitamins, fibres) are enabling product innovation across health-positioned variants, premium indulgent SKUs, and regional flavour expansion tailored to Indian palates. For instance, Amul launched high-protein milkshakes on its e-commerce platform in India, delivering 15-20 grams of protein per serving, aimed at fitness-focused urban consumers and reinforcing the shift toward functional dairy variants.Smart Packaging and Cold Chain

Tetra Pak aseptic cartons, lightweight PET bottles, and eco-friendly paper-based alternatives are expanding, alongside improved cold-chain integration through quick-commerce dark stores, which maintain temperature integrity from manufacturer to final consumer in metropolitan markets. In February 2025, Tetra Pak became the first carton packaging producer to introduce ISCC PLUS certified recycled polymer packaging to India's food and beverage industry.Market Segmentation Analysis

By Flavour

Chocolate commands a 32.6% majority share in 2025, reflecting broad appeal across age groups, strong association with indulgence and familiarity, and consistent availability across all retail channels. Vanilla (21.4%) and Strawberry (18.7%) follow as classic mainstream flavours widely accepted across Indian consumers.

To access detailed market analysis, 高清体育直播:Request Sample

Banana at 12.3% in 2025 serves both indulgent and health-positioned variants, often marketed as protein-enriched or energy-focused options. Other flavours (15.0%), including regional kesar-pista, rose, coffee, and mango, represent the fastest-growing innovation pocket, with premium brands driving experimentation and consumer trial.By Distribution Channel

Online Stores dominate at 28.4% in 2025, reflecting rapid quick-commerce expansion across Zepto, Blinkit, and Swiggy Instamart. Supermarkets and hypermarkets (26.7%) follow, supported by Reliance Smart, DMart, More, and Star Bazaar expanding chilled dairy shelves across metropolitan store formats.

Regional Market Insights

|

State |

Share (2025) |

Key Growth Drivers |

| Maharashtra | 16.8% | Mumbai-Pune urban density, quick commerce leadership, organised retail penetration |

| Karnataka | 11.1% | Bengaluru IT workforce, startup culture, premium consumption, quick commerce |

| Tamil Nadu | 9.5% | Chennai metro, strong dairy parlour network, Hatsun Arun brand reach |

| Delhi | 8.2% | NCR metropolitan consumption, quick commerce hub, Mother Dairy home market |

| Gujarat | 7.5% | Ahmedabad-Surat growth, Amul home market, strong dairy cooperative base |

| Andhra Pradesh & Telangana | 6.8% | Hyderabad IT corridor, premium consumption, organised retail expansion |

| Uttar Pradesh | 6.3% | Lucknow-Kanpur tier-2 cities, rising urban consumption, cold chain growth |

| West Bengal | 5.6% | Kolkata metro, sweet-tooth dairy culture, Mother Dairy and local brands |

| Kerala | 4.6% | High per-capita dairy consumption, Milma parlour network, tourism |

| Haryana | 3.7% | NCR dairy belt, Vita cooperative, high milk production, strong rural base. |

| Punjab | 3.2% | Verka cooperative strength, premium dairy consumption, high per-capita milk intake. |

| Rajasthan | 2.9% | Saras cooperative, Jaipur urban growth, expanding tier-2 demand. |

| Madhya Pradesh | 2.4% | Sanchi brand presence, Indore-Bhopal tier-2 expansion, rising rural consumption. |

| Bihar | 2.1% | Sudha brand reach, Patna urbanisation, improving cold chain infrastructure. |

| Orissa | 1.7% | Omfed cooperative, Bhubaneswar growth, coastal dairy demand. |

| Others | 7.6% | Jharkhand, Chhattisgarh, Uttarakhand, Himachal, J&K, North-East and remaining states. |

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

| Amul (GCMMF) | Amul Milkshake, Protein Shake, Amul Kool Shakers | Leader | National dairy scale, cooperative network, brand trust |

| Mother Dairy Fruit & Vegetable Pvt. Ltd. | Mother Dairy Milkshake | Leader | NCR dominance, organised retail, retail parlour network |

| Parle Agro | Smoodh | Leader | Packaged beverage distribution, pricing discipline |

| Britannia Industries | Britannia Winkin Cow Thick Shake | Challenger | FMCG distribution strength, retail footprint |

| HAP (Hatsun Agro Product Limited) | Arun Ice Cream Shake, Hatsun Milk Beverage | Challenger | South India dairy leadership, Arun brand equity |

| Heritage Foods Limited | Heritage Milkshakes | Emerging | South India dairy presence, retail parlours |

| Keventers | Keventers Milkshakes | Emerging | Premium thick-shake quick-service experience |

| Cream Bell (Devyani Food Industries Ltd.) | Cream Bell Milkshakes | Emerging | Retail parlour and HoReCa channel |

Key Company Profiles

Amul (GCMMF)

Amul, operated by the Gujarat Cooperative Milk Marketing Federation, is India's largest dairy brand with an extensive cooperative network spanning millions of dairy farmers and manufacturing operations across multiple states.- Product & Platform Portfolio: Amul Kool Milkshake, Amul Cool Cafe, Amul Flavoured Milk, Amul Kool Cafe Koko, retail parlour offerings.

- Recent Developments: In September 2025, GCMMF announced plans to invest ₹10,000 crore in 10-12 new dairy, ice cream, and food manufacturing plants, targeting ₹1 lakh crore turnover within 2-3 years and reinforcing its scale leadership across dairy, beverages, and packaged food categories.

- Strategic Focus: Amul prioritises scale-driven cost leadership, broad flavour portfolio covering mainstream and regional variants, affordable price points, and strong alignment with India's dairy cooperative distribution network.

Mother Dairy Fruit & Vegetable Pvt. Ltd.

Mother Dairy, a subsidiary of NDDB, is a leading dairy brand with strong presence in the National Capital Region and expanding footprint across North and East India, operating an extensive retail parlour network.- Product & Platform Portfolio: Mother Dairy Milkshake, Cool Cafe, flavoured milk variants, premium and value ranges for retail and quick commerce.

- Recent Developments: In March 2025, Mother Dairy launched its 'Pro' range of protein-centred dairy products starting with Promilk, a high-protein milk variant offering 30% more protein than regular milk.

- Strategic Focus: Mother Dairy focuses on NCR-led dairy leadership, retail parlour expansion into tier-2 cities, and premium flavour and functional variants targeting urban health-conscious consumers.

Parle Agro

Parle Agro is a leading Indian packaged beverage company, best known for Frooti and Appy, with expanding dairy beverage offerings including Smoodh targeting value-positioned flavoured milk drink segments.- Product & Platform Portfolio: Smoodh flavoured dairy drink, Frooti, Appy Fizz, and broader packaged beverage portfolio.

- Recent Developments: In February 2026, Parle Agro launched Smoodh Kesar Badam, the newest addition to its flagship dairy beverage brand, expanding the Smoodh portfolio into premium Indian flavour profiles at its signature value price point.

- Strategic Focus: Parle Agro targets affordable-indulgence positioning, aggressive distribution through its beverage network, pricing discipline at mass price points, and expanded dairy drink footprint across India.

Market Concentration Analysis

Investment & Growth Opportunities

Fastest-Growing Segments

Online-led distribution is the highest-growth sub-segment through 2034, driven by quick-commerce adoption and direct-to-consumer brand expansion. Maharashtra, Karnataka, and Delhi lead state-level growth, supported by strong urban consumption and the densest quick-commerce infrastructure.Emerging Market Expansion

Plant-based dairy alternatives, functional high-protein shakes, and regional flavour innovations are the emerging premium sub-markets. Tier-2 and tier-3 cities represent the highest-potential geographic expansion opportunity as cold-chain infrastructure and organised retail deepen across India.Venture & Private Investment Trends

Notable transactions include continued private-equity interest in premium D2C dairy beverage brands, scaling of artisanal thick-shake chains, and strategic investments by FMCG majors in functional and plant-based dairy alternatives. Start-ups in lactose-free, high-protein, and clean-label shakes are attracting Indian venture capital.Future Market Outlook (2026-2034)

Research Methodology

Primary Research

Primary research encompassed structured interviews with Indian dairy and beverage industry stakeholders, including product managers at leading manufacturers, retail chain category leads, quick-commerce platform operators, artisanal brand founders, and distributor specialists across metropolitan and tier-2 markets.Secondary Research

Secondary sources include FSSAI publications, NDDB dairy statistics, company annual reports from Amul, Mother Dairy, Parle Agro, and peer brands, retail industry trade publications, quick-commerce sector data, and Indian food and beverage conference proceedings.Forecasting Models

Market size estimations were derived using top-down and bottom-up models, incorporating urban consumption patterns, retail channel penetration data, quick-commerce category growth, and historical dairy beverage expansion trends. Scenario analysis (base, optimistic, conservative) was performed to account for input cost variability.India Milkshake Market Report Coverage

|

Attribute |

Details |

| Market Size (2025) | INR 8.93 Billion |

| Forecast Size (2034) | INR 35.57 Billion |

| CAGR (2026-2034) | 16.10% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Segmentation | By Flavour (Chocolate, Vanilla, Strawberry, Banana, Others); By Distribution Channel (Online Stores, Supermarkets and Hypermarkets, Convenience Stores, Milk Parlours, Others) |

| Regional Analysis | Maharashtra, Karnataka, Tamil Nadu, Delhi, Gujarat, Andhra Pradesh & Telangana, Uttar Pradesh, West Bengal, Kerala, Haryana, Punjab, Rajasthan, Madhya Pradesh, Bihar, Orissa, and others |

| Key Companies | Amul (GCMMF), Mother Dairy Fruit & Vegetable Pvt. Ltd., Parle Agro, Britannia Industries, HAP (Hatsun Agro Product Limited), Heritage Foods Limited, Keventers, Cream Bell (Devyani Food Industries Ltd.), etc. |

| Report Format | PDF, Excel |

| Customisation | Available on request |

Frequently Asked Questions About the India Milkshake Market Report

The India milkshake market was valued at INR 8.93 Billion in 2025, driven by urban youth consumption, quick-commerce expansion, premium flavour innovation, and 🧜rising disposable income across Indian metropolitan markets.

The market is projected to reach INR 35.57 Billion by 2034, growing at a CAGR of 16.10% du🌞ring 2026-2034, driven by quick-commerce penetration, premium flavour innovation, and tier-2 city expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302INDIA

Phone: +91-120-433-0800UNITED KINGDOM

Phone: +44-753-714-6104Email: 高清体育直播:[email protected]

Client Testimonials

.webp)